Why Do Some Companies Trade at Higher Valuation Multiples?

Companies trade at different valuation multiples due to various company-specific and external factors. At its core, multiples reflect an investor's perceived risk-adjusted returns in a company. The higher the risk, the lower the value multiple because an investor is willing to pay less for the investment to ensure a higher ultimate return. The most typical valuation multiples are price-to-earnings (P/E), enterprise value-to-sales (EV/S), and enterprise value-to-EBITDA (EV/EBITDA), which investors use to gauge the relative value of a company's stock.

The growth prospects of a company significantly influence its relative valuation. A company with strong growth potential is likely to have a higher valuation multiple, as investors are willing to pay more for the expectation of greater future earnings. The example below shows two companies (A and B) with the same EBITDA as the starting point, but one is growing significantly faster than the other. Requiring the same return on investment, you should be willing to pay more for the faster-growing company. At a comparable 30% investment yield, Company B's implied enterprise value would be significantly lower, leading to a lower multiple.

Obviously, the market rewards growth, which is reflected in a premium. If you look at current EBITDA, you would be paying a higher multiple today for Company A, but considering forward-looking multiples, then an investment in Company A may be cheaper on a relative basis.

The industry in which a company operates significantly influences its valuation multiple. Idiosyncratic risk, sector cyclicality, market saturation stage, cost structure, capital requirements, and market correlation are all industry-specific and affect how investors value companies. For example, tech companies often trade at higher multiples due to their growth and scalability, while utilities typically trade at lower multiples due to their predictable yet limited growth potential. Familiarity with industry-specific dynamics is crucial for understanding the risks-reward profile before investing in a company.

Furthermore, profitability and financial health are crucial factors impacting valuation multiples. Companies with strong and consistent profitability, healthy balance sheets, and efficient capital deployment will likely command higher multiples. Conversely, companies with volatile earnings, high debt levels, or poor cash flow generation may trade at lower multiples as investors perceive higher risk.

Finally, external factors, such as market sentiment and macroeconomic conditions, also contribute to differences in valuation multiples. For instance, higher interest rates reduce valuations and compress multiples universally but may impact certain companies or industries more. Additionally, when future earnings growth is in jeopardy during economic uncertainty, investors tend to be more cautious and value companies at lower multiples. Conversely, in optimistic market conditions, companies may be valued at higher multiples in anticipation of faster and higher earnings.

In conclusion, companies trade at different valuation multiples mainly due to growth prospects, industry dynamics, profitability, financial health, and macroeconomic factors. Understanding these factors is essential for investors seeking to make informed decisions about the relative value of different companies.

The Reasoning Behind Unlevered Free Cash Flow (and How to Calculate It)

Unlevered Free Cash Flows (UFCF) refer to the cash flow available to all equity holders and debtholders after accounting for operating expenses, capital expenditures, and investments in working capital. This theoretical corporate finance figure is crucial in financial modeling as it helps determine a company's enterprise value without considering the impact of its capital structure. In essence, it shows how much cash flow equity and debt holders can access from business operations.

To calculate a company's UFCF, we can use either EBITDA or net income as a starting point. In both cases, the first step is to arrive at EBI (earnings before interest) more commonly known as NOPAT (net operating profit after tax). EBI measures a company's profitability after tax without considering its capital structure.

If you begin with EBITDA, you can subtract depreciation, amortization, and taxes to get to EBI. Pretty straightforward.

EBI = (EBITDA - Depreciation - Amortization) * (1 - Marginal Tax Rate) or

EBI = EBIT * (1- Marginal Tax Rate)

If you start with Net Income, you must adjust for interest expense and non-recurring, non-core operation income and expenses, including the tax shield, and work your way back to EBI.

EBI = Net Income + Adjustments (net of tax shield)

Adjustments = (Interest Expense - Interest Income - Non-Operating Income + Non-Operating Expenses) x (1 - Marginal Tax Rate)

Although EBI is a valuable metric for measuring an organization's operating profitability, it does not accurately reflect cash flow. This is because EBI incorporates non-cash expenses, such as depreciation and amortization, which need to be added back. Furthermore, EBI fails to consider any changes in working capital or capital expenditures directly affecting an organization's cash flow.

The final adjustments required to arrive at the UFCF are visible in the following formula:

EBIDA = EBI + Depreciation + Amoritzation

Unlevered Free Cash Flow = EBIDA - Change in Net Working Capital - Capital Expenditures

Understanding how to calculate a company's unlevered free cash flow is crucial in financial modeling. By conducting a discounted cash flow analysis on a firm's unleveraged free cash flows, you can calculate a company's enterprise value for M&A purposes and compare its valuation to that of other similar firms.

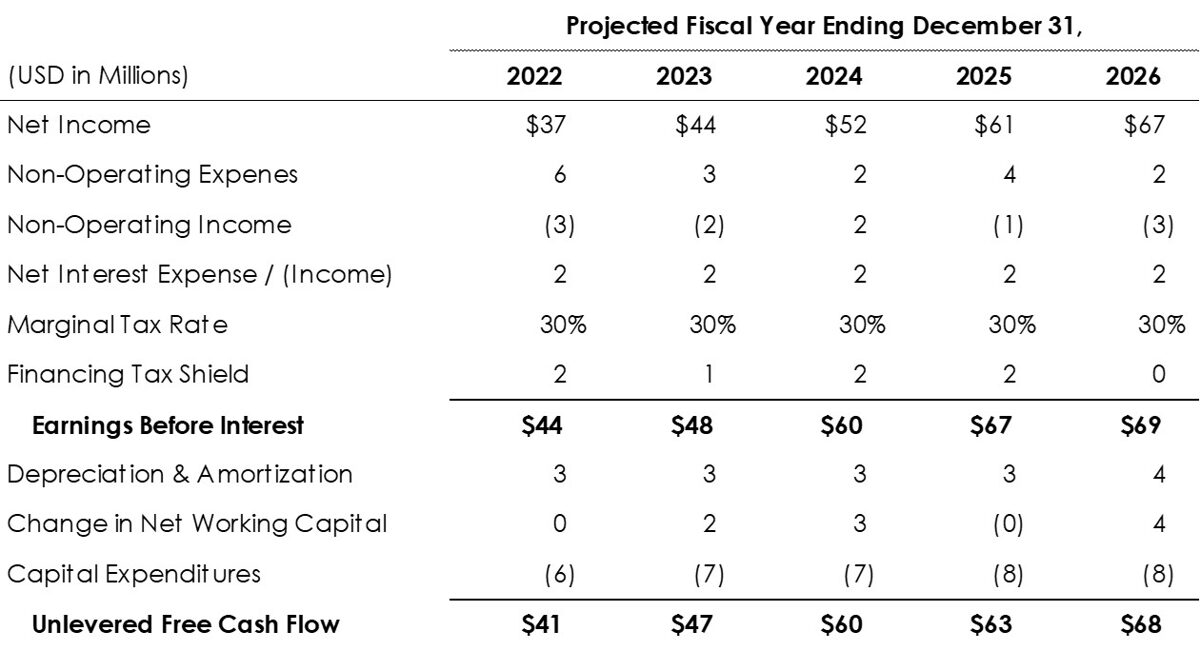

Below is an example of the how to get to unlevered free cash flow starting from net income.

Strategic vs Financial Buyers: Who To Sell To?

When selling your business, keep in mind the two kinds of buyers you can sell to: strategic or financial.

A strategic buyer is a company in your industry or related industry that wants to acquire your company for strategic reasons such as increasing market share, achieving economies of scale or entering into a new market. Most mergers occur when a company buys out a smaller competitor or niche player in the same industry.

Strategic Buyers: Pros & Cons

Strategic buyers differ from financial buyers in that they intend to integrate the new company with their existing business. For example, a regional bank might acquire a small independent bank outside its territory to expand its footprint. Its motivation for buying it isn’t purely financial like a private equity firm, which can lead them to make higher offers. However, a seller must be mindful when working with a strategic buyer, as the table below shows:

While the appeal of a strategic buyer offering more cash upfront is clear, one must be mindful of the downside scenarios. Alternatively, financial sponsors tend to offer business owners a path to maximize value alongside them.

Financial Buyers: Pros & Cons

While strategic buyers are interested in integrating sellers into their existing corporate entity, financial buyers are more interested in growing profit in the short term in preparation for an eventual sale. Naturally, this goal impacts the experience of the seller. To summarize:

When working with a private equity (PE) firm, you may have to wait longer to get paid, but the potential reward down the line could be bigger. This is why PE firms usually pay higher sale prices (cash + equity) than strategic buyers. In the last five years, this difference has become even more noticeable.

Regardless of the type of buyer, it's crucial to have a reliable M&A advisory firm to negotiate the deal. This is especially important when dealing with PE firms, which can be more complex.

Source: First Page Sage, Insead.